Oil market’s missing link is OPEC’s oil consumption!

Anas Alhajji, Contributing Editor

https://www.worldoil.com/magazine/2019/january-2019/columns/oil-and-gas-in-the-capitals

One of the most overlooked items that contributed to a soft oil market during 2018 was domestic oil demand in OPEC countries in general, the Gulf States in particular, and especially in Saudi Arabia. One important component of domestic Saudi consumption is the oil used in power generation (and diesel in private generation) during summer months, an issue discussed in this column a few times in the past. The irony is that the impact of power burn and private generation has always surprised the market with lower supplies and higher oil prices, but not in 2017–2018, when it was truly needed!

Historically, higher oil prices led to higher government spending and bigger development projects. Electricity demand grew as the number of people in urban areas increased, as a result of migration from rural areas and the growth in the number of expatriates. The peak summer demand started breaking records, and with it, power burn increased, leading to smaller-than-expected net exports.

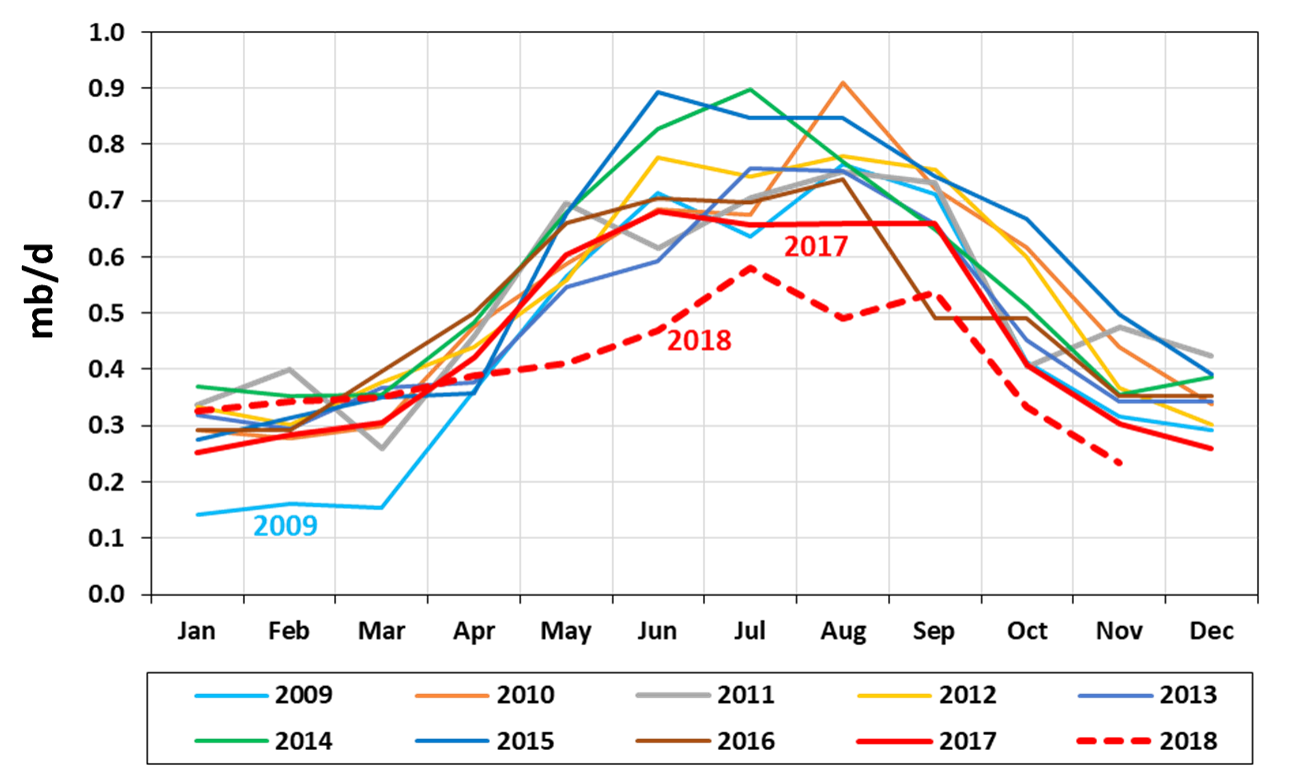

As the chart below shows, Saudi power burn declined drastically in the last two years. Higher oil prices in 2018 should have stimulated economic activities and increased power burn, but it did not. Why?

Four major policy changes led to this decrease in Saudi domestic oil consumption, freeing more oil for exports, as follows.

An exodus of expatriates, mostly middle- and higher-income expats, who resided in the country with their families. Cities moved from a shortage of housing and office space to a major surplus. Real estate prices declined drastically, as vacancies of housing and office space soared. The exodus was the result of a government policy that aimed at reducing the number of expatriates and replacing them with Saudi nationals. The government instituted high fees and taxes that made it difficult for expatriates to keep their families in Saudi Arabia, and sometimes for the expats, themselves, to stay.

A major reduction in energy subsidies that increased electricity bills substantially, while it raised transportation fuel prices. The impact on peak electricity demand and transportation fuel consumption was large, despite government programs to subsidize households below a certain income level. Higher energy prices cause a price effect and an income effect. Government payments compensated only for the income effect. The net was a decline in demand

Slow economic growth on lower oil prices on one hand, and restructuring of the economy on the other. The impact of the exodus of expatriates on the housing and retail industries, and their impact on economic growth, cannot be ignored. The impact of low oil prices on domestic power burn can be seen in the first quarter of 2009, during the financial crisis, when oil prices collapsed.

New energy efficiency programs that aimed at reducing wastage and improving energy use, especially in air-conditioning and appliances. Air-conditioning, alone, uses 70% of total electricity consumption in Saudi Arabia. Any efficiency gains translate into a noticeable decline in electricity usage. More efficiency gains are expected, as the Energy STAR program is better managed and enforced in the coming years.

Saudi Power Burn Declined in 2017 and 2018

Source: JODI, 2018. November’s number is author’s estimate.

On a separate but related matter, Saudi Arabia increased its natural gas production in the last two years and aims to double its gas output during the next 10 years. This increase will enable Saudi Arabia to free the electricity sector from oil use, export the freed oil without any additional investment, reduce emissions, and provide enough energy for the industrial sector and mega data centers that are part of the 2030 Vision.

The 2019 Saudi Budget. The Saudi government announced its 2019 budget on Dec. 18, 2018. Despite relatively low oil prices, it was the largest budget ever: $295 billion. This expansionary budget was needed to stimulate the economy, lower unemployment, and set the basic infrastructure needed for Vision 2030. Although the budget came with a deficit of 4.2% of GDP, it was lower than the deficit in 2017, which was 9.3% of GDP.

The average yearly oil price needed to finance the revenues has been estimated around $70/bbl. This is not the price needed to balance the budget. A few comments are in order:

The oil-producing countries’ budget break-even oil prices that some media outlets, and some research centers, are fascinated with are irrelevant and have never been relevant to the oil market.

Theoretically, what matters to the oil market is only the oil price that is used to “finance” revenues in the Saudi budget. Saudi Arabia is the only country that can influence the oil market by being a swing producer. The belief here is that Saudi Arabia will adjust production to where the assumed price that finances revenues becomes a price floor in the global oil market.

But practically, oil producers, including Saudi Arabia, are flexible. They can withdraw money from foreign reserves, cut spending, delay or cancel projects, and borrow from domestic and international markets.

Therefore, the $70 price needed to finance revenues becomes a guide post to what the government of Saudi Arabia wants as a minimum price, but if markets overpower Saudi Arabia, the Kingdom can manage its finances through different means. The irony here is that the higher the price desired by the Saudis, the happier the free riders are. Will we see an average Brent price of $70/bbl next year? According to several forecasts, yes, although others are lower, but too close. Price volatility will decline, if Saudi Arabia defends the price floor, but several factors might prevent the Kingdom from doing so, leading to higher volatility. wo

{kind=link}

Comment